In 2026, your compliance department is no longer a back-office cost center; it’s the primary engine driving your corporate bank account approval in the UAE. Since the UAE’s removal from the FATF Grey List in February 2024, regulatory scrutiny has reached a new peak, making internal oversight your most critical asset. You likely feel that managing Anti-Money Laundering (AML) and Economic Substance Regulations (ESR) is a constant struggle against a moving target. It’s exhausting to watch your expansion stall because a local bank rejects your application due to perceived risks or missing frameworks.

We understand that you want to focus on growth, not paperwork. This guide promises to simplify these complex requirements by providing a clear roadmap for building a robust compliance department that secures your business license and ensures banking success. You’ll learn how to implement a structured guidance system that satisfies the Central Bank of the UAE and protects your firm from the heavy fines that impacted 24 percent of non-compliant firms in the previous fiscal year. We are moving from mere administrative setup to a future-driven strategy that guarantees your long-term security in the region.

Key Takeaways

- Learn how to transform your compliance department from a reactive watchdog into a proactive strategic asset that anticipates regulatory shifts in the 2026 landscape.

- Discover the five essential pillars required to map your industry’s legal landscape and prevent violations before they impact your business operations.

- Master the nuances of the UAE’s stringent AML and KYC frameworks to ensure seamless banking approvals and long-term corporate license security.

- Gain a step-by-step blueprint for drafting a bespoke compliance manual and fostering a culture of integrity within your growing SME.

- Explore how to simplify complex UAE regulations into actionable growth steps through a professional, future-driven strategic partnership.

What is a Compliance Department in the 2026 Business Landscape?

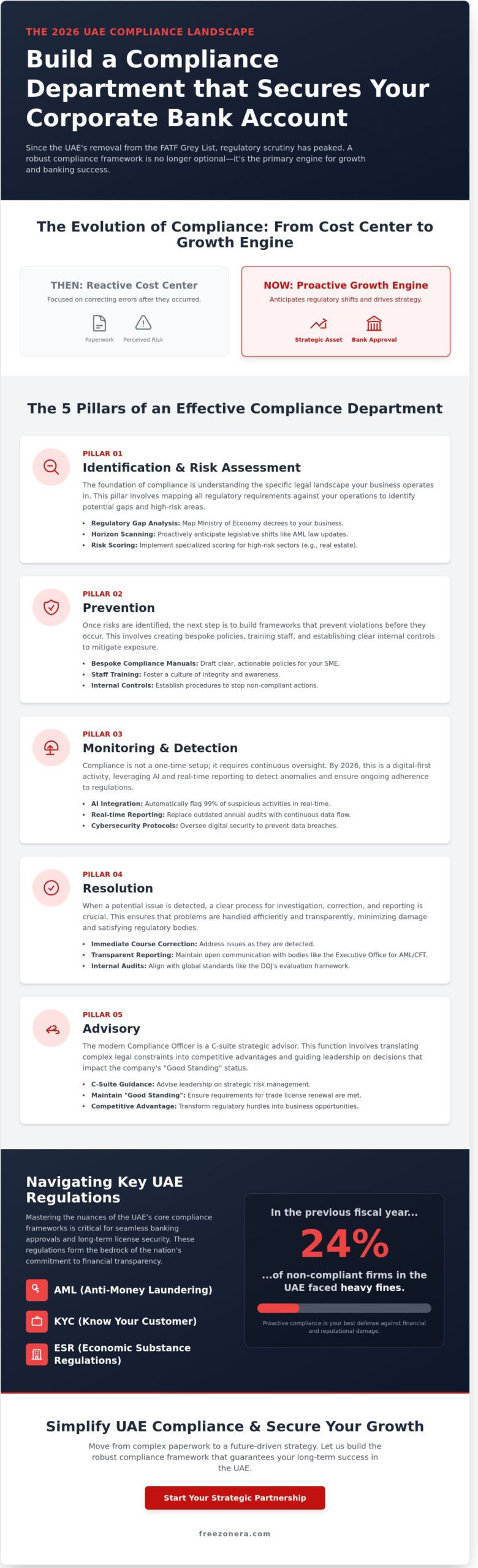

A compliance department acts as the internal guardian of a firm’s legal and ethical standards. By 2026, this unit has evolved into a strategic hub that ensures every transaction and corporate action aligns with the UAE’s sophisticated legal framework. It’s no longer just a back-office function. It’s a proactive center for strategic risk management that protects a company’s reputation and operational license. This department bridges the gap between internal operational controls and external regulatory bodies like the Ministry of Economy and the Central Bank of the UAE.

The shift from reactive “policing” to proactive strategy is now the industry standard. Previously, compliance teams focused on correcting errors after they appeared in annual reports. Today, they use predictive analytics to identify risks before they manifest. This transition is essential because Regulatory compliance has become a 24/7 automated requirement in the UAE’s digital economy. Businesses must maintain constant vigilance to stay ahead of rapid legislative updates across mainland and free zone jurisdictions.

The Evolution of the Compliance Officer

The Compliance Officer has moved from an administrative clerk role to a C-suite strategic advisor. This professional is now vital for maintaining a company’s “Good Standing,” a status required for renewing trade licenses and securing corporate banking facilities. Without this expert oversight, entrepreneurs risk losing their operational permits in a market that prioritizes transparency. The modern Compliance Officer is a navigator of regulatory complexity who transforms legal constraints into competitive advantages.

Why 2026 Demands a Digital-First Approach

Digital transformation has redefined the daily operations of the compliance department. Integration of AI is now the standard for monitoring high-volume transactions and identifying anomalies that suggest financial crime. In 2026, real-time reporting has replaced traditional annual audits in most modern jurisdictions. This allows for immediate course correction and ensures total transparency with the Executive Office for AML/CFT.

- AI Integration: Automated systems now flag 99% of suspicious activities in real-time, reducing human error.

- Data Privacy: Strict adherence to the UAE Federal Decree-Law No. 45 of 2021 on Personal Data Protection is a core remit.

- Cybersecurity: Compliance teams now oversee digital security protocols to prevent data breaches and ensure business continuity.

This digital-first strategy simplifies complex processes for both startups and established firms. It ensures that clarity and compliance aren’t just goals but are embedded into the daily operational rhythm of the business. By leveraging these tools, companies can focus on growth while the compliance framework provides a steady, secure foundation for future-driven success.

The Five Pillars of an Effective Compliance Department

A robust compliance department functions as the architectural backbone of a resilient UAE enterprise. By 2026, the complexity of the regional regulatory environment, particularly within DIFC and ADGM jurisdictions, demands a structured approach. An effective framework relies on five fundamental pillars that transform legal obligations into operational advantages: identification, prevention, monitoring, resolution, and advisory functions. To ensure these pillars meet international benchmarks, many firms now align their internal audits with the DOJ’s Evaluation of Corporate Compliance Programs, which provides a globally recognized standard for program efficacy and resource allocation.

Identification and Risk Assessment

Success starts with a meticulous regulatory gap analysis. For an entrepreneur entering the UAE market, this means mapping every decree from the Ministry of Economy against current operational capacity. Your compliance department must perform “horizon scanning” to anticipate legislative shifts, such as the 2024 updates to the UAE’s Anti-Money Laundering (AML) laws. This proactive stance identifies high-risk areas in cross-border financial transactions before they trigger administrative penalties. High-risk sectors, including real estate and precious metals, require specialized risk scoring to prevent unintended exposure to sanctioned entities or illicit cash flows.

Monitoring and Detection Strategies

Continuous oversight replaces periodic checks in a modern corporate setup. Companies now utilize Key Risk Indicators (KRIs) to trigger automated alerts when transaction patterns deviate from established norms. Data from 2025 industry reports indicated that 68% of corporate fraud cases were detected through internal reporting mechanisms rather than external audits. This highlights the necessity of robust whistleblower policies that protect anonymity and encourage internal accountability. Detection is only effective when paired with a culture of transparency. Without an environment where employees feel safe reporting anomalies, even the most advanced automated systems will fail to catch nuanced ethical breaches.

The final pillars, resolution and advisory, ensure the business remains agile. Resolution requires pre-defined protocols to address breaches within 48 hours of discovery, minimizing reputational damage. Simultaneously, the advisory pillar positions compliance officers as strategic partners rather than bureaucratic hurdles. They provide the legal roadmap for new ventures, ensuring that expansion into digital assets or “Smart Manufacturing” remains within the bounds of UAE law. If you’re looking to simplify your business setup while maintaining these rigorous standards, professional guidance ensures your framework is future-proof and fully aligned with 2026 mandates.

Compliance in the UAE: Navigating AML, KYC, and ESR

The UAE regulatory landscape shifted significantly following the nation’s exit from the FATF “Grey List” in February 2024. This milestone solidified the country’s status as a secure global financial hub, but it also raised the bar for corporate transparency. Your compliance department must now master the Federal Decree-Law No. (20) of 2018 on Anti-Money Laundering. This framework isn’t just a suggestion; it’s a rigorous mandate that requires constant vigilance. A functioning compliance department acts as your first line of defense, ensuring that every transaction and partnership remains above board.

Securing “Know Your Customer” (KYC) approval is the most critical hurdle for operational continuity. Compliance officers verify identities, map the source of funds, and ensure that every stakeholder meets international standards. Beyond identity, businesses must navigate Economic Substance Regulations (ESR). If your entity performs “Relevant Activities” like banking, insurance, or investment management, you’re required to prove actual economic activity within the UAE. Additionally, Ultimate Beneficial Owner (UBO) declarations are non-negotiable. Failing to maintain an accurate UBO register can lead to administrative penalties starting at AED 15,000, making it a priority for any structured entity.

Securing UAE Corporate Banking through Compliance

Opening a bank account is often the toughest challenge for new entrepreneurs. Industry data shows that UAE banks reject nearly 50% of corporate applications because of incomplete or poorly structured compliance documentation. Banks are inherently risk-averse; they require absolute clarity. A dedicated compliance file speeds up this process by organizing business plans, invoices, and supplier contracts into a professional package. Integrating these standards into your UAE Company Setup 2026 strategy ensures that your path to a functional business account is clear. It’s about building trust with financial institutions through precision and transparency.

Free Zone vs. Mainland Compliance Requirements

Compliance obligations vary depending on your jurisdiction. Free Zones like RAKEZ and DMCC have specific digital portals for reporting and annual audits. These jurisdictions operate with high levels of autonomy but strictly adhere to federal AML standards. Mainland companies, however, interface directly with the Ministry of Economy. They must register on systems like the GoAML portal to report suspicious transactions in real-time. Since the UAE’s exit from the Grey List, regulators focus on the quality of reporting rather than just the presence of a policy. Whether you’re in a specialized hub or the heart of Dubai, your internal processes must reflect this shift toward global excellence. Consistency is the only way to avoid the heavy fines associated with non-compliance.

How to Build a Compliance Framework for Your SME

SMEs in the UAE often view a compliance department as a luxury reserved for multinational corporations. This is a misconception. A lean, effective framework protects your license and builds investor trust. You don’t need a massive team to be compliant; you need a structured system that scales with your growth. Start by defining your risk profile based on your specific license activity, whether you operate in a free zone or on the mainland.

Drafting Your Compliance Manual

Your manual serves as the operational blueprint. It must include a Code of Conduct, Anti-Money Laundering (AML) policies, and Data Protection protocols aligned with Federal Decree-Law No. 45 of 2021. This manual isn’t a static file for the shelf. It’s a living document. Update it every six months to stay ahead of evolving UAE Central Bank and Ministry of Economy regulations. Localized legal review is non-negotiable. Regulations in the Dubai International Financial Centre (DIFC) differ significantly from those in the Abu Dhabi Global Market (ADGM) or mainland jurisdictions.

Structure your framework with these essential pillars:

- Mandatory Training: Conduct quarterly workshops to instill a “Culture of Compliance.” 100% staff participation ensures everyone understands their personal liability.

- Internal Audit Schedule: Set a recurring 90-day calendar for policy reviews. This identifies gaps before they lead to regulatory fines.

- RegTech Integration: Use automated KYC (Know Your Customer) tools. These systems can reduce manual screening errors by up to 45% while fitting within a modest SME budget.

The Build vs. Outsource Debate

Deciding whether to hire an in-house officer or partner with a consultancy depends on your current scale. Startups often face high overheads when hiring full-time specialists. Outsourcing provides immediate access to “Sophisticated Navigator” expertise without the long-term salary commitment. This approach is particularly effective for navigating the 2024 AML updates that require specialized reporting knowledge. For firms with over 50 employees or those in high-risk sectors like fintech, a hybrid model often works best. It combines internal oversight with external strategic guidance. This ensures your compliance department remains agile and future-driven.

Ready to secure your business’s future and avoid regulatory hurdles? Simplify your UAE compliance journey with FreezonEra’s expert guidance.

Simplifying UAE Compliance: The Freezonera Advantage

Entering the UAE market requires more than just a trade license; it demands a robust framework for long-term survival. Freezonera acts as your strategic partner, transforming the complex duties of a traditional compliance department into a streamlined, manageable process. We don’t just provide checklists. We provide a “Simplification” philosophy that breaks down the 2026 regulatory environment into actionable steps for every entrepreneur.

Our approach removes the friction from market entry. By 2023, the UAE Ministry of Economy had already intensified inspections, resulting in significant fines for businesses lacking proper AML and ESR documentation. We ensure your venture isn’t part of those statistics. Our team anticipates these hurdles before they impact your operations, allowing you to focus on growth while we handle the regulatory heavy lifting.

From Formation to Financial Success

Success in the UAE depends on how well you integrate compliance into your initial licensing process. We don’t treat setup and regulation as separate entities. Instead, we embed mandatory standards into your company’s DNA from day one. This proactive stance is vital when dealing with the UAE’s sophisticated banking sector.

Local and international banks, including entities like Emirates NBD and Wio, have strict compliance expectations that often catch new founders off guard. We bridge this gap through our established network of banking partners. By providing structured guidance, we ensure your documentation meets the high-bar requirements of 2026 financial institutions. This significantly reduces the risk of account delays or rejected applications, which can stall a business for months.

This integrated approach offers three distinct benefits:

- Regulatory Alignment: Your license structure is chosen specifically to satisfy future audit requirements.

- Document Readiness: We prepare “bank-ready” dossiers that anticipate the KYC (Know Your Customer) queries of 2026.

- Operational Clarity: You receive a clear roadmap of your ongoing obligations, from VAT filings to corporate tax submissions.

Your Next Steps for a Compliant UAE Future

Waiting for a violation notice is the most expensive compliance strategy a business can adopt. In the UAE, administrative penalties for failing to maintain accurate Ultimate Beneficial Ownership (UBO) registers can be severe. Professional regulatory oversight isn’t just a safety net; it’s a competitive advantage that provides peace of mind.

Future-proofing your business means staying ahead of evolving laws like Corporate Tax and the latest VARA updates for digital assets. Freezonera offers the steady hand you need to navigate these shifts. Don’t leave your corporate standing to chance. Simplify your UAE compliance and business setup today with Freezonera and build a legacy backed by expert precision.

Future-Proof Your UAE Operations Through Strategic Governance

Navigating the UAE’s regulatory landscape in 2026 requires more than just basic administrative awareness. It demands a proactive approach to AML and KYC standards established by the UAE Ministry of Economy. Your compliance department acts as the essential backbone of this strategy; it transforms rigid legal obligations into a clear competitive advantage. By 2026, businesses operating within jurisdictions like DMCC and RAKEZ must adhere to even stricter ESR reporting cycles to maintain their standing.

You don’t have to manage these evolving complexities in isolation. Freezonera offers a structured guidance system that bridges the gap between traditional setup and future-driven digital growth. Our team brings a proven track record in simplifying Mainland, RAKEZ, and DMCC requirements for international entrepreneurs. We combine technical expertise with a holistic approach to ensure your venture remains both secure and scalable. Secure your business future with Freezonera’s expert compliance and setup services. Let’s build a resilient foundation for your long-term success today.

Frequently Asked Questions

What is the primary function of a compliance department?

The primary function of a compliance department is to ensure that a business operates within the legal frameworks set by UAE regulatory bodies like the Central Bank or the Ministry of Economy. This department identifies risks and implements internal controls to prevent violations of Federal Decree-Law No. 20 of 2018. It acts as a shield, protecting the company from legal penalties while maintaining operational integrity across all business activities.

Is a compliance department mandatory for small companies in the UAE?

Whether it’s mandatory depends on your specific business activity. For Designated Non-Financial Businesses and Professions (DNFBPs), such as real estate agents or precious metal dealers, having a compliance function is a legal requirement under the UAE’s 2021 AML regulations. Small companies in these sectors must register on the goAML portal and appoint a compliance officer to avoid fines starting from AED 50,000.

How does a compliance department help with opening a UAE bank account?

A compliance department simplifies the bank account opening process by preparing a comprehensive Know Your Customer (KYC) file that meets strict UAE Central Bank standards. By pre-vetting your corporate documents and source of wealth, they reduce the likelihood of application rejection. Banks are 40 percent more likely to approve accounts when they see a structured compliance framework already in place within the applicant’s business structure.

What is the difference between a legal department and a compliance department?

The legal department focuses on interpreting laws and managing contracts, while the compliance department ensures the business follows those laws in daily operations. Think of legal as the architects who understand the building codes and compliance as the site managers who ensure every brick is laid according to those codes. In the UAE, legal handles litigation risks, whereas compliance focuses on regulatory adherence to prevent fines.

What are the risks of not having a compliance department?

Companies without a dedicated compliance department face severe risks, including administrative fines that can reach AED 5 million under UAE Cabinet Decision No. 16 of 2021. Beyond financial loss, you risk the immediate suspension of your trade license or being blacklisted by financial institutions. These penalties often lead to permanent reputational damage, making it nearly impossible to secure future partnerships or international contracts within the UAE market.

How often should a company conduct a compliance audit?

You should conduct a formal compliance audit at least once every 12 months to align with the UAE’s annual financial reporting cycles. However, the introduction of the UAE Corporate Tax Law in June 2023 makes more frequent quarterly reviews necessary for many firms. Regular checks ensure your business stays ahead of legislative updates and identifies potential gaps before they become costly regulatory violations or operational bottlenecks.

What is AML and KYC in the context of UAE business?

AML stands for Anti-Money Laundering, and KYC refers to Know Your Customer protocols. These are the two pillars of UAE financial security regulated by Federal Decree-Law No. 20 of 2018. AML involves the processes used to prevent illegal funds from entering the financial system. KYC is the mandatory verification of a client’s identity and financial background to ensure they don’t pose a risk to the business.

Can I outsource my compliance department functions in the UAE?

You can absolutely outsource your compliance functions to specialized consultancies in the UAE. This approach is often more cost-effective for startups and SMEs that don’t need a full-time, in-house team. Professional firms provide the necessary expertise and stay updated on the latest 2026 regulatory changes. This allows you to focus on growth while experts handle the complex administrative tasks required by UAE authorities.