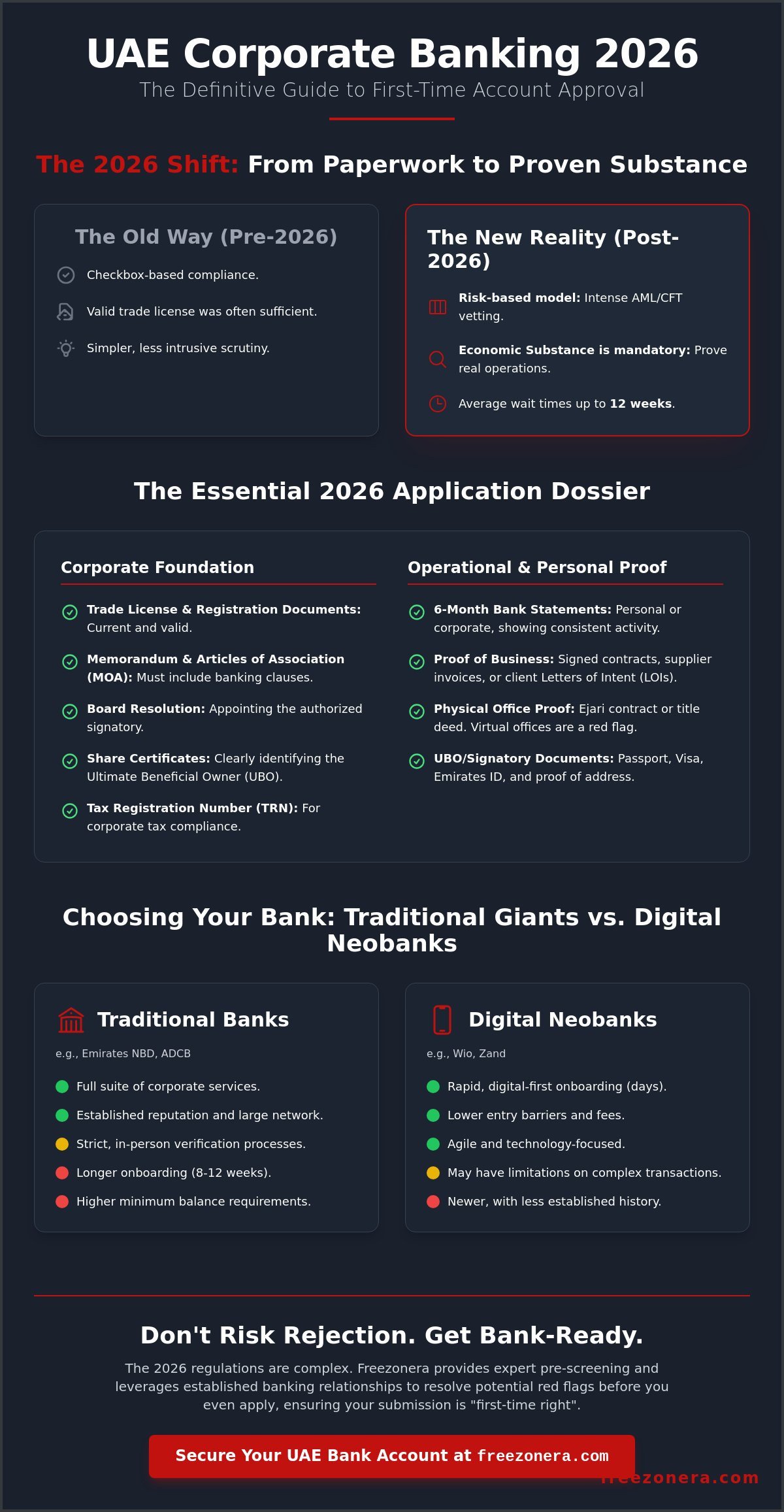

In 2026, holding a valid trade license is no longer a guaranteed ticket to a business account in the UAE. Following the Central Bank’s April 16, 2026, mandate on stricter AML and CFT guidance, banks have shifted from checkbox compliance to a rigorous risk-based model. You’ve likely felt the frustration of waiting up to 12 weeks only to receive a rejection without a clear explanation. We understand that meeting the corporate bank account opening Dubai requirements can feel like aiming at a moving target while your capital sits idle.

It doesn’t have to be a process of trial and error. This guide provides the definitive 2026 checklist to help you secure a first-time right approval by proving your economic substance and transaction transparency. You’ll learn how to navigate the 9% corporate tax landscape, choose between traditional giants like Emirates NBD and agile neobanks like Wio, and prepare the specific documentation that satisfies today’s heightened scrutiny. We’re here to simplify the complex and get your operations running without the typical administrative lag.

Key Takeaways

- Understand how the April 2026 CBUAE updates have shifted the focus toward economic substance, making transparency more critical than ever for approval.

- Identify the specific legal and personal documentation needed to satisfy corporate bank account opening Dubai requirements, ensuring a “first-time right” submission.

- Learn the strategy for building a “bank-ready” profile that highlights your supply chain transparency and passes the initial compliance filter.

- Compare the benefits of traditional institutional banking against the rapid onboarding offered by UAE neobanks like Wio and Zand.

- Discover how professional pre-screening and established banking relationships can resolve potential red flags before they lead to an application rejection.

The 2026 Banking Landscape: Why Dubai Corporate Account Requirements Are Stricter

The Central Bank of the UAE (CBUAE) fundamentally altered the regulatory environment on April 16, 2026. This date marked the introduction of stricter Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT) guidance. For entrepreneurs, this means the banking landscape in the UAE is now defined by transparency rather than just paperwork. Compliance is no longer a static event; it’s a continuous lifecycle that requires active management.

Meeting the corporate bank account opening Dubai requirements now demands a clear demonstration of economic substance. Banks have moved away from a one-size-fits-all checklist. Instead, compliance officers employ a risk-based approach. They scrutinize every layer of your ownership structure and your specific business activities. If your company lacks clear operations or relies on a complex web of offshore entities, it’s often flagged as a shell company. In 2026, these entities are essentially unbankable because they represent a high risk for Proliferation Financing (PF) and Trade-Based Money Laundering (TBML).

The introduction of the 15% minimum tax for large multinationals on January 1, 2025, further aligned the UAE with global OECD standards. This global alignment means local banks must be more vigilant than ever. If you’re concerned about how these changes affect your setup, you can reach out to us for structured guidance and pre-screening support.

The Evolution of Economic Substance Regulations (ESR)

Substance isn’t just a legal term; it’s a physical reality. A verifiable commercial space is now a non-negotiable requirement for most traditional banks. Compliance teams often verify your physical presence through Ejari contracts or by requesting site visits to your office in Dubai or Ras Al Khaimah. The days of using a simple postal box address are over. To secure an account, you must show that your business is managed and directed from within the UAE jurisdiction.

Corporate Tax and Banking Synergy

The federal corporate tax, which introduced a 9% rate for income above AED 375,000, has created a new layer of bank oversight. Your Tax Registration Number (TRN) is now a core requirement for account maintenance. Banks use your tax filings to verify that your revenue matches your declared business activity. This synergy ensures that only legitimate, tax-compliant businesses remain active. Preparing for annual reviews is essential, as banks now require verified financial statements to maintain your corporate facility.

The Essential 2026 Corporate Bank Account Opening Checklist

Precision is mandatory for a successful application. While a standard trade license is the foundation of your business, banks now demand a comprehensive look into your operational history and your professional credibility. Meeting the corporate bank account opening Dubai requirements in 2026 involves assembling a dossier that proves both your legal existence and your commercial intent. Compliance officers prioritize the clarity of your corporate structure. This level of scrutiny is detailed in recent industry reports regarding Corporate Bank Account Opening in Dubai 2026, which highlight the shift toward verified, high-quality documentation.

You’ll need to provide six months of bank statements, either personal or corporate, from your home country or an existing entity. These statements must show consistent activity; dormant accounts are a major red flag. Additionally, operational proof is no longer optional. Banks expect to see signed contracts with suppliers or formal letters of intent from potential UAE clients. If your documentation feels incomplete, you can consult our compliance specialists to ensure every box is checked before submission.

Core Corporate Documentation

Your Memorandum and Articles of Association (MOA) must be current and explicitly include banking clauses that authorize the opening and management of accounts. A formal Board Resolution is also required to appoint the specific authorized signatory who will handle the account. In the 2026 regulatory environment, share certificates must clearly trace the Ultimate Beneficial Owner (UBO). Banks will reject applications where the ownership structure is opaque or involves multiple layers of holding companies without a clear individual at the top.

Personal KYC for Shareholders

Know Your Customer (KYC) protocols have become significantly more personal. You must provide a proof of residential address, such as a utility bill or a bank statement, that isn’t older than three months. A major addition to the 2026 checklist is the “CV Requirement.” Banks now analyze your professional background to ensure you have the necessary experience in the industry you’re entering. This helps them assess the risk of business failure. Finally, ensure all documents from outside the UAE are notarized and apostilled according to the latest 2026 standards to avoid immediate rejection at the intake stage.

KYC and AML: Proving Your Business Legitimacy to Compliance

In 2026, passing the initial compliance filter requires more than a stack of papers. It requires a narrative that aligns with the Central Bank of the UAE regulations. Most rejections occur because the applicant’s business model appears vague or disconnected from their professional history. To meet the corporate bank account opening Dubai requirements, you must present a ‘Bank-Ready’ Business Profile. This document serves as your company’s resume, translating your commercial goals into terms a compliance officer understands. It’s the bridge between having a license and actually having an active account.

Transparency in your supply chain is non-negotiable. You’ll need to identify your top five anticipated customers and suppliers. Banks use this data to perform background checks on your trading partners. If any of these entities are linked to high-risk jurisdictions or sanctioned countries, your application will likely stall. Be realistic with your transaction projections. While it’s tempting to forecast high volumes, compliance officers prefer conservative, data-backed estimates that match your initial deposit capacity. If you’re unsure how to structure your source of wealth disclosure, you can consult our compliance team for a pre-submission review.

Crafting the Business Profile

Your profile must provide a detailed description of business activities that match your trade license exactly. Ambiguity is a major red flag. You should clearly state your anticipated monthly turnover and initial deposit amounts. Additionally, provide a list of target countries for inbound and outbound transfers. Following the April 16, 2026, CBUAE updates, banks specifically look for potential exposure to Trade-Based Money Laundering. Providing this information upfront demonstrates that you’re an organized, low-risk client.

Ultimate Beneficial Owner (UBO) Transparency

Complex holding structures are under intense scrutiny. If your structure involves multiple layers of offshore holding companies, expect the vetting process to extend by several weeks as officers trace the path of every dirham back to its origin. You’ll need to disclose your source of wealth, explaining exactly how you funded your new UAE venture. This might involve providing tax returns or inheritance documents from your home country. Preparing for the compliance interview is the final hurdle. Expect questions about your industry experience and your reasons for choosing a specific UAE jurisdiction. Clear, honest answers are your best tool for securing approval.

Choosing the Right Bank: Traditional vs. Digital Neobanks

Selecting a financial partner is a strategic decision that depends entirely on your business model and operational needs. In 2026, the corporate bank account opening Dubai requirements vary significantly between established giants and agile digital players. Traditional institutions like Emirates NBD or Abu Dhabi Commercial Bank (ADCB) offer a sense of permanence and a dedicated relationship manager. These banks usually require a minimum average monthly balance of AED 50,000 for their standard corporate accounts, with non-maintenance fees reaching up to AED 400 per month. For businesses requiring high-level credit facilities, these traditional giants remain the primary choice.

Conversely, the rise of UAE neobanks has transformed the market for startups and SMEs. The UAE’s FinTech market is projected to reach $179 billion by 2026, and digital-first banks are leading this growth. Wio Bank, which serves over 120,000 business clients as of early 2026, offers zero-balance accounts in exchange for monthly subscription fees ranging from AED 99 to AED 250. While digital banks provide rapid onboarding, they often lack the physical infrastructure required for high-volume cash deposits. Crucially, some neobanks cannot issue the specific “Bank Reference Letter” often required for certain UAE residency visas. If you’re struggling to decide which route fits your growth plan, get in touch with Freezonera for a tailored banking assessment.

When to Choose a Traditional Bank

Traditional banks remain the gold standard for companies with complex trade finance needs. If your operations require Letters of Credit (LCs) or Bank Guarantees, a traditional relationship is essential. These banks also allow you to establish a long-term credit history, which is vital if you plan to apply for corporate mortgages or expansion loans later. They provide a physical point of contact, which is often reassuring for entrepreneurs navigating the UAE’s administrative landscape for the first time.

The Neobank Advantage for Startups

Neobanks like Mashreq NeoBiz and Zand are built for speed and efficiency. They often finalize account opening in 48 hours to 7 days, compared to the 4 to 12 weeks seen at traditional institutions. These platforms excel at API integrations, making them the preferred choice for e-commerce and digital-first businesses. They eliminate the need for in-person visits, which is a significant advantage for international entrepreneurs who haven’t yet secured their physical residency.

Simplifying the Process: How Freezonera Navigates Your Opening

Successfully meeting the corporate bank account opening Dubai requirements in 2026 demands more than a complete dossier. It requires a strategic alignment between your corporate structure and the current risk appetite of UAE financial institutions. At Freezonera, we act as your sophisticated navigator, ensuring your application is bank-ready before it ever reaches a compliance officer’s desk. We identify potential red flags, such as opaque ownership layers or high-risk jurisdictions, allowing you to address these issues proactively. This pre-screening process is vital in a year where rejection rates have climbed following the Central Bank’s April 2026 regulatory shift.

Our expertise isn’t limited to paperwork. We specialize in customizing your UAE company setup to meet specific banking preferences from the start. This includes selecting the right jurisdiction and trade license activities that banks currently favor as low-risk. Once your account is active, our support continues to ensure your facility remains in good standing. We help you maintain compliance through the annual reviews and tax filing requirements that are now standard in the 2026 financial environment. Our goal is to prevent the account freezing that often occurs when entrepreneurs overlook secondary compliance deadlines.

Structured Guidance from Setup to Banking

Your trade license activity is the first thing a bank evaluates during onboarding. We ensure your activities are classified correctly to avoid immediate exclusion from traditional banking channels. Additionally, we assist in securing physical office space that satisfies the stringent economic substance requirements mentioned earlier in this guide. For those managing global interests, we coordinate with Worldwide Formations in Dubai to streamline cross-border banking complexities. This ensures your international footprint doesn’t trigger unnecessary compliance alerts during the vetting process.

Ready to Start Your Dubai Business Journey?

The 2026 market values clarity and compliance above all else. Attempting to handle the application process alone often leads to the 12-week delays and unexplained rejections that plague many entrepreneurs. By leveraging our established relationships with UAE banking compliance departments, you significantly reduce your rejection risk. We provide the structured guidance needed to turn a potentially overwhelming bureaucratic process into a predictable path to operational success. Precision is our signature. Reach out to Freezonera for expert banking support and secure your company’s financial future today.

Secure Your Business Future in the UAE

The shift toward economic substance and stricter AML protocols in 2026 has made the banking process more technical, but it remains a manageable hurdle with the right preparation. You’ve seen how choosing between a traditional institution and a digital neobank depends on your specific credit needs and transaction volumes. Most importantly, ensuring your documentation reflects a transparent business model is the only way to avoid the common 12-week processing delays. Meeting the corporate bank account opening Dubai requirements is about precision, not just the volume of paperwork.

With expertise across 40+ UAE Free Zones and strategic partnerships with the country’s leading banks, Freezonera provides a structured guidance system that works. Our 95% application success rate for pre-screened clients shows that rejections are preventable when you address red flags early. Simplify your corporate bank account opening with Freezonera and gain the clarity you need to start operating. We’re ready to help you build a future-driven business in Dubai’s thriving economy.

Frequently Asked Questions

Can I open a corporate bank account in Dubai without a residency visa?

You generally cannot open a traditional corporate account without a residency visa for the authorized signatory. Most banks require an Emirates ID to complete the mandatory Know Your Customer (KYC) process. While some neobanks offer restricted services to non-resident shareholders, the primary account operator must hold a valid UAE residency permit to satisfy the 2026 corporate bank account opening Dubai requirements.

How long does it take to open a business bank account in the UAE in 2026?

Processing times vary significantly based on the institution you select. Digital neobanks like Wio often finalize accounts within 48 hours to 7 days. In contrast, traditional banks usually take between 4 and 12 weeks due to the rigorous 2026 AML and CFT vetting processes. Complex ownership structures involving offshore holding companies can extend this timeline by an additional 4 weeks.

What is the minimum balance required for a corporate account in Dubai?

Minimum balance requirements range from zero to over AED 500,000. Neobanks often offer zero-balance accounts in exchange for a monthly subscription fee. Traditional banks like Emirates NBD or Mashreq usually require a minimum average monthly balance of AED 50,000 for basic business accounts. Premium corporate tiers may demand maintained balances of AED 250,000 or higher to avoid monthly penalties.

Why do UAE banks reject corporate account applications so frequently?

Rejections often stem from a lack of “Economic Substance” or vague business models. Banks frequently flag applications that involve high-risk jurisdictions or lack a physical office presence. Since the April 16, 2026, Central Bank update, applications are also rejected if transaction projections don’t align with the shareholder’s documented professional background or proven source of wealth.

Do I need a physical office to open a corporate bank account in Dubai?

A physical office is now a core requirement for most traditional banking institutions. While some neobanks accept virtual office addresses, traditional compliance officers often request a verified Ejari lease contract for a physical commercial space. This helps prove your business is managed from within the UAE, which is a critical part of the corporate bank account opening Dubai requirements in 2026.

Can a Free Zone company open a bank account in a Dubai Mainland bank?

Yes, a Free Zone company can open an account with a Dubai Mainland bank. UAE banks are licensed federally, allowing them to serve clients across all jurisdictions, including mainland, free zone, and offshore. However, the bank will still evaluate your specific license activity to determine if it fits their internal risk appetite for the 2026 financial year.

What happens if my corporate bank account application is rejected?

If your application is rejected, you should first request a meeting with your relationship manager, though banks aren’t legally obligated to disclose specific reasons. Your next step is to re-evaluate your business profile for red flags before applying to a different institution. Repeatedly applying with the same flawed documentation can lead to a “blacklisting” effect across the local banking sector.

Is it possible to open a UAE corporate bank account remotely?

Remote opening is possible through digital neobanks that use biometric verification via mobile apps. However, traditional banks almost always require at least one in-person visit by the authorized signatory to finalize the application. This visit is necessary for the bank to verify original passports and witness the signing of the account opening forms as required by 2026 CBUAE regulations.